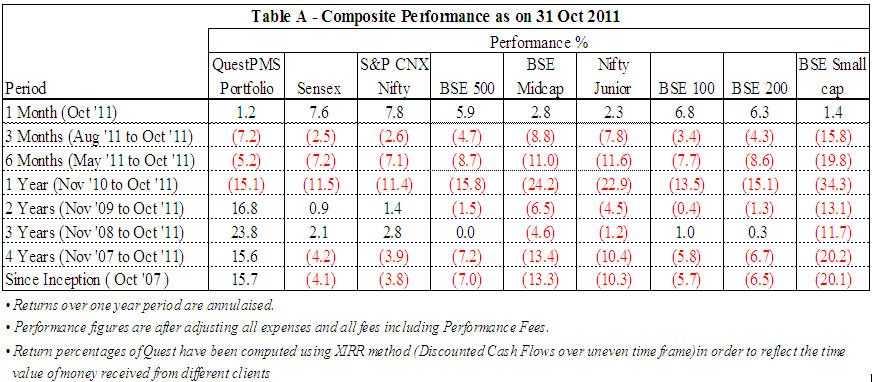

Opportunity in a challenging environmentA resilient Indian MarketThe international news flow during the month was dominated by the problems in Eurozone and weak economic indicators in the US. By the end of October, policymakers in Europe announced a write down of Greece’s sovereign debt, a package for recapitalizing European banks and leveraging the European Financial Stability Facility (EFSF) upto USD 1.5 trillion. This alleviated markets obsession with the problems in Eurozone, atleast in the short term. On the domestic front, RBI’s repeated monetary tightening measures have not been successful in controlling inflation. Despite this, the RBI governor announced a further hike in policy rates and, also freed interest rates on savings account. However, there was an indication that RBI is likely to pause its rate tightening measures. This may have been influenced by two factors: First, the government’s borrowing programme will be higher than budgeted. Second, industrial production data revealed that increase in interest rates was beginning to have an impact on corporates. Indian companies were postponing investment plans: this was also clear from the lower than expected growth in advances by the banking sector. The market participants were also looking forward to the Q2FY12 results. A quick look at the consolidated performance of 500 companies shows that the profit growth has been the slowest in the last five quarters. Despite this, the markets have shown resilience with most of the benchmark indices rising by almost 1-8% during the month. Foreign investors are sanguineIt is striking that the recent market turbulence has not triggered a large-scale pull-out by foreign institutional investors (FIIs), unlike in 2008 when the FIIs withdrew ~US$12bn from the Indian markets. While the Sensex has fallen ~15% from its November 2010 highs, data released by the exchanges suggest it is not the FIIs, but Indian retail investors, that have done most of the selling. Not that the FIIs haven’t had any provocation to head the exit door. Concern over a slower recovery in the US, likely sovereign defaults in Europe and political uprisings in the Arab world could have prompted capital flight away from risky assets (such as emerging markets). Specifically on India: a nationwide anti-corruption mood and newfound regulatory activism stemming from the unearthing of a series of scams, has led to a near-standstill in policymaking. That has, in turn, dampened investment confidence, even as Indian corporates have seen a sharp deceleration in earnings momentum due to rising interest rates, forex losses, higher wages and increase in other input costs. That the FIIs have remained marginal net buyers despite all this probably represents a residual hope, even if not a ringing vote of confidence, about India’s long-term growth story. The FIIs seem more sanguine than domestic retail investors and, there might be some positive takeaways from the recent stability in FII flows. One, it could signify a changed perception among FIIs: Indian stocks represent a reasonable long-term investment rather than a risky short-term trading bet. To that extent they believe that the problems that are stalling India’s economic growth are not structurally insurmountable. Second, the basic profile of foreign portfolio investors itself may have undergone a change. In 2007-08, it was hedge funds, keen to make quick gains from each market move that dominated the scene. Today, the ones cropping up most in the list of foreign investors are exchange traded funds, emerging market mutual funds and pension funds that have a longer investment horizon. The situation for the Multinational Corporations (MNC) is somewhat different from portfolio investors. As I mentioned in my earlier letter, MNCs are holding record levels of cash and are likely to use this to begin serious conversations for acquiring targets. As there are limited high-quality targets in emerging markets, first movers will gain an advantage over competitors in terms of quality of assets as well as valuations. A decline in share prices offers an opportunity to MNC companies to put in place their merger & acquisitions strategies and, simultaneously pursue a plan to delist the shares of Indian subsidiaries. But India has to address challengesTwo years ago, when the developed world was seeking growth opportunities in the emerging markets, India missed the opportunity to secure foreign investments desperately needed to get its infrastructure act together. Appropriate and timely policy action could have attracted both debt and equity investors: with near zero interest rates in developed economies, debt capital was cheap and, equity investors in those countries were also desperate for the higher returns available in the faster growth countries of Asia. Today, the government runs the risk of being too late – at least for now. The cost of capital is going up and, most investors are in risk-averse mode. The recent calm on the FII front should be no reason for complacency. It provides a short window of opportunity for the Government to resolve critical growth-crippling bottlenecks in power, coal, transport and other infrastructure, besides pushing ahead with long-pending reforms in retail, energy pricing, labour, finance and agriculture. If it fails, FIIs may well find other emerging markets offering better growth prospects. Asian countries will drive global growthAfter four years into the global economic crisis, most accept that the underlying problem is one of solvency and not liquidity – solvency of banks and solvency of countries, especially in the Eurozone. Experts expect that things in Asia will get better after a few months but the rest of the world may remain impacted for over a decade. Performance of QuestPMSOn October 12, 2011, QuestPMS completed four years. While markets have declined marginally during past 4 years, QuestPMS has delivered 15.7% annualized compounded returns after all expenses and fees since inception (see table A). The QuestPMS portfolio has 20 companies (mostly midcaps) with an average turnover being ~Rs.2,150 crores. The average market capitalization of companies in the portfolio is ~Rs.3,230 crore. Taken together, the companies in QuestPMS are totally debt free. Also on average, these companies have cash that is 17 per cent of the market capitalization. At current prices, the QuestPMS portfolio companies are trading at a weighted average PE multiple of 13.0 times expected FY12 EPS and 9.8 times expected FY13 EPS. The recovery in the market during October 2011 has been driven by investors buying into the large cap stocks and, ignoring opportunities in mid cap companies. This reflects the preference of investors who are seeking safety in “liquid” stocks and turning away from “value” stocks further widening the valuation gap. As I have mentioned earlier, our philosophy is to take a long-term view and, at times, accept the short term under performance. It has been my experience that it is during such times, a disciplined and an unwavering approach to investments is likely to be rewarded generously.

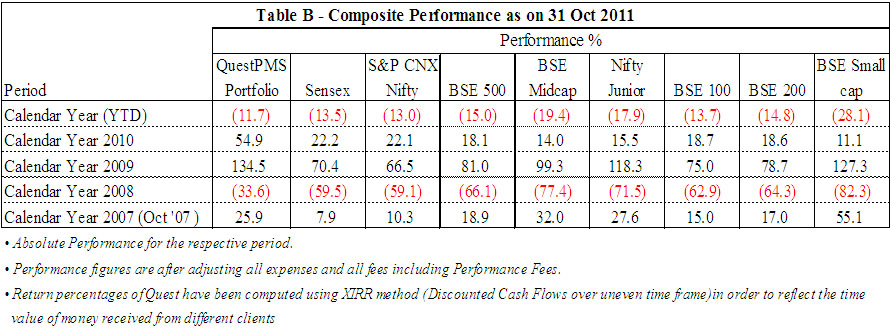

I tried to evaluate our performance during good times, bad times and during the time where market was going nowhere. As the accompanied table B indicates that while we performed exceedingly well in good times of 2007 and 2009 (calendar year basis), the erosion in QuestPMS was much lower during bad times of 2008 and 2011. The performance was exceptionally good during steady year of 2010.

And all this was possible as my team remained committed to its knitting with conviction and discipline during good times and bad times. ConclusionI have chosen to sum up my argument on “Opportunities in a challenging environment” with an extract from a recent statement by Deepak Parekh, Chairman HDFC – “A 7 per cent expected GDP for the current year is not good for me…We had an excellent monsoon; agricultural output is going to be at an all-time high. But there are some hindrances in terms of some policy changes and some policy paralysis. If we get over them, I am sure we can achieve 7.5 to 8 per cent growth rate…It’s a reality that emerging countries are going to be new leaders in the global economy. Almost 40 per cent of world’s population lives in India and China. And these two countries are expected to witness consumption-led growth….That’s why India is on the radar of every big MNC. I think every big MNC has realized that if it doesn’t invest in India now, it will regret in the long run. True, it is a bit difficult to do business in India. But once you establish yourself, there is no looking back.” While it is true that the present investment climate looks quite hazy and things may change over the next few months, in my opinion, the present moment is the most appropriate time for stock picking. Just like good times do not last forever, bad times also pass. At times, investors have unrealistic expectations. They believe it is possible to time the markets and, weave in and out of various assets classes on time, every time. I believe that this is possible in dreams and, mostly remains in the domain beyond the consciousness. But not many are willing to accept this. Making market forecasts is becoming increasingly difficult, as it now entails an understanding of US politics, Chinese monetary and financial policy, Greek and Italian attitudes and German elections in addition to the usual economics, corporate developments and actions and comments by FED and RBI. Many a times, I have observed that a sharp decline in share prices of fundamentally strong companies is not related to corporate developments or weakening fundamentals. That does not, of course, mitigate the pain of seeing those and other stocks fall, but it suggests that the pressure is more probably temporary than enduring. I do not know how and when all this will end. I take this opportunity to reiterate that my team at QuestPMS will continue with its time-tested investment strategy which rests on identifying companies with a scalable business model backed by a good management and are available at an absolutely reasonable price (and importantly, staying invested even if there are disappointments in the interim). I hope the festival of light and the New Year ushers in happiness and prosperity for the investing community. With best wishes to you and family for the festive season, Ajay Sheth October 31, 2011 To know more about Quest and QuestPMS please visit our website: www.questinvest.com DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Ajay Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |