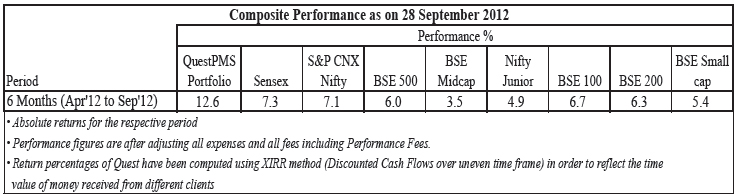

Economic reforms supported by Global Liquidity – a potent combination“Good returns are seldom made on investments made in good times. Rather, good returns are typically made on investments made in adverse times”. Just before the festivities to welcome Lord Ganesh began, Dr Manmohan Singh’s government announced bold steps, surprising everyone. It seemed that the Lord had cleared the Vignas Whatever the calculations, the steps announced by the government in the middle of September 2012 infused life into the markets. These also coincided with the announcement by the Federal Despite the negatives faced by the Indian economy (high inflation, high interest rates, high fiscal and current account deficit, scams, corruption scandals, a non-functioning of Parliament, absence of reforms, etc.), the stock markets have remained reasonably strong. During the quarter July to September 2012, major indices have gained 7 to 9 per cent largely on the strength of continued investments by FIIs ~Rs.34,700 crores(source: BSE website). Since the beginning of 2012, for the 9-month period ended September 2012, FIIs have invested ~Rs.74,000 crores in Indian equities. In contrast, the domestic institutions have been sellers – having sold equities worth ~Rs.38,000 crores(source: BSE website). Investments by FIIs have gained momentum due to policy announcements since mid September and, expectations of additional policy reforms over the next few months. QE3 – truly a game-changer Globally major economies (USA, Europe and Japan) are in the middle of a recession and their central bankers are willing to do anything to come out of this situation. In order to boost Last fortnight, Fed announces a unique QE3. Compared to the two previous QEs (Quantitative Easing), this one is unlimited. While the earlier two were for fixed amounts, under QE3, every What are the probable effects? The Fed is encouraging people to put their money anywhere but in cash. Neither cash nor short-term bonds offer any yield or any defence against inflation. The Fed is encouraging everyone to buy anything that gives a yield, such as high-yield bonds or high dividend paying stocks. Whether this move will stimulate the job market is debatable. But there is one lesson that we cannot ignore: over the past three years, the Fed has been able to move asset prices. Apart from the Fed, European Central Bank’s Draghi has announced unlimited bond buying. Japan is also on the same path. Someone has rightly quipped: “Never argue with liquidity”. Kick-starting Reforms In an abrupt change in stance and risking its own survival, the government announces a series of politically contentious policy changes that seek to kick-start economic reforms. In a span of two days, it took multiple decisions to rejuvenate India’s economic fortunes. First, it hiked diesel price and put a cap on use of subsidized LPG cylinders cutting down subsidy bill by Rs.20,000 crores. Next, it allowed 51 per cent FDI in multi-brand retail, 100 per cent FDI in single brand retail, 49 per cent FDI in aviation and 74 per cent FDI in cable and (direct to home) DTH operations. And lastly, it announced a fresh round of disinvestment of PSU shares which will allow it to raise Rs.30,000 crores. Ever since late 2010 when the 2G spectrum scandal stormed into the public domain, fears of political losses kept the government from taking the right steps. With a potential sovereign More Reforms to come? To capitalize on the momentum generated by the mid-September big-bang announcements, the government has hinted at more policy announcements over the next 8 to 12 weeks. Many of On the government’s agenda is also implementation of the Shome Committee report that has recommended abolition of both short term and long-term capital gain tax on all listed equities Considerable improvement in Monsoon The late pick up in the southwest monsoon has wiped out a large part of the deficit from almost all regions across the country. This has increased availability of drinking water, reduced fodder deficit, improved prospects of the kharif crop and, enhanced the possibility of a substantially higher rabi crop. A buoyant agri-economy should help to sustain rural demand. Core inflation and repo rate to fall According to Crisil, with investment demand nearly stagnating and private consumption growth falling to a 10-year low of 4 per cent in Q1FY13, the current elevated levels of core inflation may not sustain beyond the next few months as prices begin to adjust to lower demand pressures with a lag. In the short term, the upward pressure on global crude oil prices as well as revision of electricity and diesel prices will reflect in higher fuel inflation. A surge in global liquidity driven by QE3 could exert pressure on commodity prices in the short run. However, the rise in commodity prices may not be sustainable in the backdrop of slowing global demand. This should benefit India that is a net importer of commodities. With domestic demand continuing to remain subdued, pressure on core inflation too should begin to moderate early next year. In this scenario, if the reform momentum continues Challenges ahead After these announcements, India may have come back on the radar of many foreign investors but there is still a need to create a confidence in the minds of the investors on many factors. The system to allocate natural resources needs to be revamped to alleviate fears of favouritism (and corruption); Indian economy is still plagued by high inflation and interest rates, among other things. There is need for further reforms, especially in areas of allocation of coal, mines, land acquisition, environmental issues and the power sector. Besides this, the government needs to further reduce subsidy on food and fertilizers. There is also a need to promote investment and enthuse confidence among businessmen. While permitting FDI in retail and insurance may help the economy on the margins, but it will not take India back to 8 per cent economic growth rate. In the short term, high crude and commodity prices due to QE could pose a risk by increasing the inflation and fiscal deficit. To add to these challenges – the government is on a knife-edge after one of its major ally Trinamool Congress walked out of the coalition. For survival, it is now dependent on parties that have a poor track record on reliability and predictability. Performance of QuestPMS “A majority of investments in equities are not done with a long term view, despite the fact that the best equities have to offer is only over long periods”. After a non-too-encouraging performance for the last financial year, QuestPMS has performed well during the six months ended April-September 2012.

However, the performance for the trailing one year and two years is below the overall performance for longer perriods. As reported in our June newsletter, this is due to the natural exclusion of two of our better quarterly performances i.e. for April-June 2011 and July-Sept 2011 from the relevant period. The anomaly may continue for the next one year due to the inclusion/exclusion of a specific quarter in the rolling one year period. The XIRR method of computing portfolio returns is also impacted by the inflow/outflow of funds. We are confident that in next two quarters, the performance of QuestPMS will return to its long term trend.

As mentioned in our last newsletter, whenever domestic investors’ apathy is witnessed, losses on small cap are on poor volumes and conversely, it is true that the share prices of these stocks appreciates faster whenever investors’ interest returns. We have utilized the current market conditions to furthur strengthen our portfolio. Most of the companies in the QuestPMS portfolio are doing very well and, we expect the performance of QuestPMS to revert to its long term trend. Inflection point in India’s dirty political economy While it is easy to get disheartened by scams such as the 2G spectrum allocation, coal crisis, Sahara ruling etc., there is a positive side. Due to indefatigable work of activists, public debate and, an active judiciary and group of investigators, politicians and big business houses are feeling the heat. India can use this opportunity to begin the clean up of the process of allocation of resources and, India’s transformation can then be for real. The poison coming out can be seen as a form of cleansing, not as a sign of greater disease. There is a possibility that the process of allocation of natural resources or auctioning of 2G licences will undergo a change and, a change for better. Untapped potential of India’s rural economy Before concluding, we have reproduced two paragraphs from the speech that Harish Manwani, Chairman of Hindustan Unilever Limited delivered at the company’s AGM on July 23rd, 2012. These provide an indication of the potential of Indian economy. – By 2025, the Indian rural market is expected to grow mare than ten-fold to become as USD 100 billion opportunity for retail spending. The key drivers for this amazing transformation are India’s accelerated consumption-led growth, significant improvement in infrastructure & communication, and increased government spending on programmes for rural development – The population of rural India is about 12 per cent of the world population, which makes it bigger than the size of Europe. It is not an impossible vision of rural India matching rural China in 10 years time. This could potentially create an incremental GDP of USD 1.8 trillion, the size of the current Indian economy. Conclusion In the words of Nido Qubein, a businessman and a motivational speaker “The present does not determine where you go; it merely determines where you start” It is likely to be tug-of-war between a surplus in global liquidity on the one hand and, economic performance (read reforms and proper economic management) on the other hand. This should awaken the animal spirits in industry leaders who may become more confident to invest in capacity creation. A global system that is awash with cheap funds and is hungry for growth can easily be attracted to India if we push ahead with some meaningful reforms. This could become a potent lethal combination and, push equity markets to levels that are above their previous highs. This will allow companies to raise funds, repait their balance sheets and expand. Moreover, the dollar inflows will boost the INR, which in turn will lead to lower imported inflation. This is what happened during the last boom. Aditya Puri of HDFC Bank has aptly summarized the current situation in India: “We are always fond of self flagellation. We do it a bit too much. Is there a concern? Yes. Is there an amount of concern as we express internally? I would say No. So, if India is to solve its problems, it would be a great country. Even otherwise, it is growing. Is there and overarching concern? I would say No. But, I think the bigger point is that we should not be in this situation. We should be a star. And what they (read foreigners) are looking at and, even if we can show some progress there – on the fiscal deficit, on the subsidies, on the tax and on easing the bureaucracy – I think you will have investments flooding in. So my view is that we are creating a crisis out of nothing. It is our view that is better to remain invested in fundamentally sound businesses. It is not the time to be extremely bold but it also not the time to be extremely cautious. To conclude, structurally India’s growth story is still intact. There is no reason for despair. We remain committed to investing for the long term, even as we reming ourselves : “It is never a great stratergy to argue with liquidity or sweet talk by policy makers.” Warm regards, Ajay Sheth September 28, 2012 To know more about Quest and QuestPMS please visit our website: www.questinvest.com DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Ajay Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |