Building a portfolio that can endure global volatility

The interlinkages between global markets and the resultant volatility has increased significantly since the financial crisis in 2008. This has been further accentuated by the uncertainty prevailing around the future of European Union since 2012-13 and more recently by the significant slowdown that has been witnessed in China. Easy monetary policy being followed across the developed world has not been able to address the slowing growth issues. Recent ‘Brexit’ vote has created fresh uncertainty in the global financial markets. Volatility levels have further increased with markets swinging from one extreme to another and sharp declines being followed by equally swift recoveries.

In the midst of these global challenges, India has doubled its GDP from USD 1 trillion to USD 2 trillion.This would obviously mean that many Indian companies have benefited from and contributed to this doubling of the economy over the last 7-8 years. Further, the Indian GDP is again estimated to more than double over the next 10 years and this too will have a significant impact on and contribution from a large number of companies. We believe that while global market volatility is the ‘new normal’ for the foreseeable future, economies like India that have a strong domestic economy will finally chart their own course. Global events such as ‘Brexit’ may have a short term impact (and provide entry opportunities!) but will not change the overall direction in the medium and long term.

Indian markets have shown remarkable resilience to global volatility in the last few months. This has been helped by better than expected Q4FY16 results, prospects of a good monsoon and continued government thrust towards reform and liberalization measures. We believe that key to generating superior returns for investors is bottom up stock-picking. Focusing on companies that have strong fundamentals, are well placed to benefit from structural changes in the Indian economy and can endure global volatility is key to building a portfolio that can outperform the markets. This has been the singular focus at QuestPMS, helping us meet and hopefully beat our investors’ expectations!

QuestPMS Performance

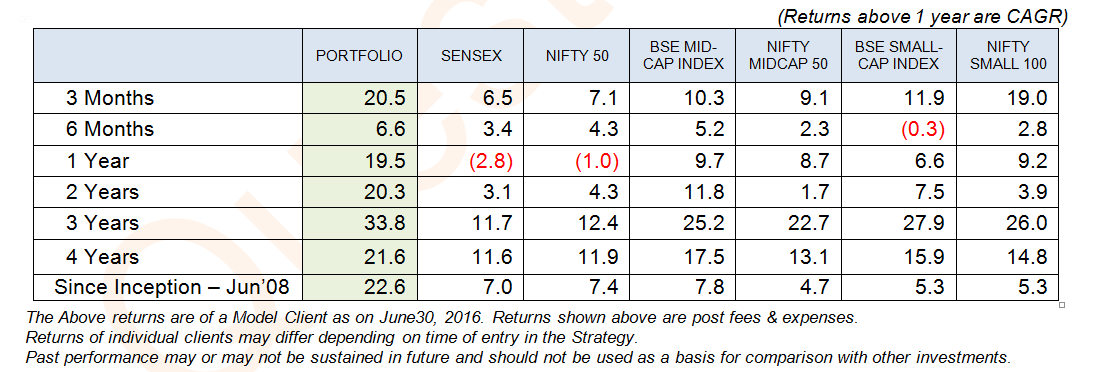

QuestPMS has done exceedingly well during the last 3 months. For the quarter ended June 2016, QuestPMS has posted a return of 20.5%, significantly outperforming most market indices.

In the last 8 years, QuestPMS has delivered an annualized compounded return of over 22% post fees and expenses versus mid-single digit returns for market indices, an outperformance of ~15% p.a.

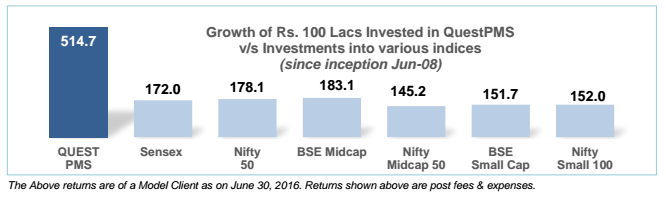

As seen from the above graph, in absolute terms, Rs.1.0 crore invested in QuestPMS in June 2008 is worth Rs.5.14 crore as on June 30, 2016 whereas the same investment in SENSEX and Nifty50 is worth Rs. 1.72 crore and Rs.1.78 crore respectively.

QuestPMS has been able to deliver superior returns mainly due to its philosophy of investing in quality growth companies at an absolutely reasonable price. At Quest, our constant endeavour is to look for companies which were in an investment phase / were experiencing slower growth / lower margins vis-à-vis their long term averages and are likely to come out of this phase and move to the next level of growth and profitability. As these companies transition into the next phase of growth, it leads to much faster EPS growth as well as PE rerating resulting in improved price performance going forward.

It is this stock picking ability that differentiates QuestPMS from others. For example, in the case of Biocon, where substantial R&D investment was overlooked by the market, rigorous monitoring of developments helped us make the investment decision when Biocon was likely to witness significant improvement in its business outlook. Our thesis on improving visibility of biosimilar business has worked out well and the stock has moved up ~60% from our averagebuy price within a short period of time. Similarly, we believe that our portfolio companies linked to the infrastructure / construction space such as Ramco Cement, KEC and Kalpataru are very well poised to increase their earnings significantly over the next few years. These companies are very well managed and will benefit hugely from rising investment in roads, irrigation, transmission and railway sectors.

Quest PMS portfolio is expected to deliver earnings growth of ~29% CAGRover the next 3 years i.e. FY16-FY19. Still, it is trading at a price earnings ratio of 15 and 12 on FY17 and FY18 basis giving us confidence in the strength of the portfolio and its ability to outperform the market in future as well.

India getting closer to a broad based economic recovery

The macro economic environment has been conducive for over 18 months now. This has been supplemented by reform and liberalization measures by the government. There has been significant increase in FDI and public investment over the last 15-18 months and the same is expected to further accelerate in the coming months.Despite this, broad based recovery in India has been elusive. Consumption demand has been weak and private investment is yet to show signs of improvement. Two consecutive monsoon failures and slowing global growth have been key to slower than anticipated recovery, apart from the fact that the NDA government inherited an economy battered by corruption scandals and policy paralysis. Also, cleaning up of bank’s balance sheet (right thing to do from medium term perspective) has reduced liquidity considerably and has created short term stress and challenges with respect to kick-starting the investment cycle.

However, it seems the aforesaid issues are now waning, clearing the path for a broad based economic recovery. IMD and other national and international agencies have predicted above average rainfall this year and La Nina prospects for next year as well. There is significant increase in transparency at the policy level and the government is much more responsive to the genuine demands of the industry.In our interactions with reputed corporate houses, we are increasingly seeing a growing sense of optimism.Also, well managed companies have become more efficient due to significant cost cutting done by them in the last couple of years. Corporate earnings in Q4FY16 have been better than expectations and this trend should continue going forward.

We are already witnessing increasing level of activity in many areas. Pace of road construction and laying of transmission lines has increased and should further improve going forward. Higher freight traffic, growth in air travel and increasing occupancy at hotels are early indicators of economy turning for the better in the last few months.With cabinet approving 7th Pay commission recommendations, there will be significant increase in disposable income in the hands of government employees.

Once there is pick-up in demand, earnings which are at cyclical lows currently, can see disproportionate rise due to operating leverage in the system. Good monsoon can bring down food inflation and create room for further cut in interest rates, thus improving cost and availability of funds. Prospects of sharp increase in earnings due to operating and financial leverage can lead to analysts revisiting their EPS forecasts resulting in rerating of Indian stocks.Indeed, there are good reasons to believe that India is at the start of a long period of growth for equities.

Risks to outlook

The most critical risk for India relates to the third consecutive failure of monsoons, a risk that has not materialized in over 100 years. Another deficient monsoon can result in untold misery and distress in the rural areas forcing the government (and probably rightly so if such a risk materializes) to focus all its efforts and resources in that direction at the cost of other important initiatives of the government.

Besides the prevailing uncertainty in EU, unexpected results in US Presidential elections, aggressive rate hikes by the Federal Reserve(though the probability of the same has further abated), further slowdown in China and sharp depreciation of the Chinese Yuan are the other risks that the global financial markets will have to contend with in the remaining part of this year. Yuan has depreciated to ~6.65 vs the dollar in the aftermath of the ‘Brexit’ vote, which is a 5 year low for the Chinese currency.

Final Thoughts

The main triggers for the return of optimism in the Indian markets in the last few months have been stabilization of commodity prices, better than expected Q4FY16 corporate earnings, prospects of a good monsoon and increasing probability of GST Bill getting throughthe Rajya Sabha hurdle this year. However, there are several fundamental reasons to believe that India is at the start of a long period of growth for equities. These include:

– Inflation and interest rates transitioning from double digits to single digits;

– Significantly enhanced image of India in the global community resulted in sharp upsurge in FDI;

– Likely improvement in corporate margins going forward;

– Proactive government measures towards policy reforms and ease of doing business;

– Under-leveraged status of Indians.This can enable consumption to rise faster than income;

– Supportive demographics, conducive for both economic growth and financial savings;

– Still very low allocation towards equities by Indians.

In the last 18 months, despite continued volatility in global financial markets, domestic investors have come back into equities. We feel this is a structural shift into financial assets, linked to demographics, lower inflation &interest rates, weakness in physical assets and improving business environment in India. However, we are still underweight equities; this shift into equities can continue for many years.

We believe that if the government is able to meticulously execute its announced plans and monsoons are favourable, we should see abroad based revival of the Indian economy by the end of this year. Also, we believe that global volatility will continue in the foreseeable future;however, if we are diligent and disciplined in building our portfolio and pick up companies that have strong fundamentals and can endure global volatility, stock prices will take care of themselves!

Bharat Sheth

June 30, 2016

DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Bharat Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and, are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them.