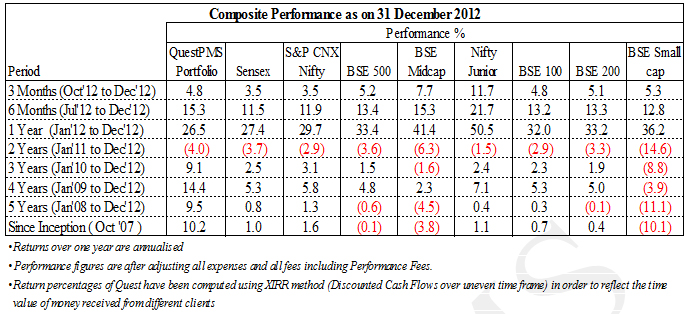

Valuation rally played out, earnings rally to play out nextOver the past one year, our investors will recall that we have always been bullish despite a gloomy scenario that was being projected all around. In December 2011 we concluded: “I am optimistic that the twilight on the sky is the beginning of dawn” and, in September 2012: “it is never a great strategy to argue with global liquidity combined with government sweet talks that is desperate to reform the economy”. Why were we bullish? Ever since 2008, when crisis hit Europe and the US, global central bankers have consistently adopted an extremely easy money policy. In a bid to revive growth in their respective economies, the Central banks provided cheap and low cost money. This low cost money was looking for growth and, countries like India that were growing, albeit at a much slower pace than in the past few years benefited from these inflows. And the result: FIIs have poured over US$ 24 billion (nearly Rs.130,000 crores) in the Indian stock market that has pushed up leading indices by more than 25 per cent in calendar year 2012. And, this is despite a gloomy scenario and sentiment amongst domestic investors: in addition to the direct selling by retail investors, the domestic institutions have sold more than Rs.56,000 crores of equities. A strong stock market performance is usually correlated with economic growth. At times, it may also be driven by low real interest rates. Neither of these two factors has been in play in India in the past 12 months and, yet it’s been a terrific year for those investors who have chosen to remain invested in equity. All this seems absurd when seen in the context of the high inflation in the economy, low growth, record fiscal and current account deficits, political instability and policy inactions. As KV Kamath, non-executive Chairman of Infosys and ICICI Bank says: “The way markets have gone up in last one year, it looks like the markets (you may read as FII) believes more in the story of India than India (you may read this as domestic institutions who have continuously sold) does or our entrepreneurs do and, so I always respect the market. The market looks at the momentum, the aspirations and, understands that there is no option but to meet the aspirations of the people and that whoever has to get things right, will get it right in due course. That’s what’s making money flow into the country”. At the risk of repeating, we do not have the skills to forecast the indices but we can look at the factors that can influence the markets and assess their impact. Fed’s additional easing Albert Einstein once defined insanity as “doing the same experiment over and over again, expecting a different result”. QE1. QE2. QE3….. Need we say more? In December 2012, the US Federal Reserve announced that it will purchase US$45 billion of US treasuries every month starting January 2013. These are in addition to the open ended monthly purchase of US$ 40 billion mortgage backed securities under the QE 3 program. The Fed has also indicated that it will keep policy rates at very low level for the next two years. In likelihood, this could ensure continuity to the “risk-on” rally on the back of significant money flowing into countries like India. While there are signs that the worst for the Indian economy is probably over, nobody is predicting a big economic rebound. In our view, the valuation based rally in the market has played out in the last one year. With economic indicators almost at the rock bottom, we expect the market to be driven by an improvement in earnings over the next 12 months. It will be a confluence of liquidity, sentiment, reforms and global cues over next 12 months and we believe, India is well placed on most of the parameters. India’s reform debate Exactly a year after the government’s big defeat came a big victory. Last December, when the government gave up its plan to allow FDI in retail, the reforms and growth agenda in the country seemed to hit a low. To the government’s credit, it recovered and secured a mandate from both houses of Parliament to allow FDI in retail. It is even more heartening that the Congress Party (read Sonia Gandhi) has publicly started to support market liberalization. While FDI in retail might look symbolic, what is important is rather than preferring to push the problem under the carpet, the government, with support from the Congress party, fought back and won. Last fortnight, it also approved a new law for land acquisition and, set up a new body to speed up clearing infrastructure projects in an attempt to kick start economic growth. Most are hoping that the government will use the new found momentum to prepare for bigger reforms like implementation of GAAR, DTC and GST. Whenever these are implemented, these reforms will be major game-changers. The Finance Minister has already gone on record that a bitter pill is needed to restore economic health. This may mean hike in petro and power prices thereby reducing government’s subsidy bill. Lower oil prices to be the biggest boon for India As a large importer of oil, high crude prices create are the biggest drain on the Indian economy. The additional funds available from Q3 have not had any major impact on crude oil prices and, the prices have stabilized in the last 3 to 6 months. Due to a combination of a surge in US crude production and weakening global economic growth, crude oil prices are likely to remain subdued. This bodes extremely well for India and the Indian economy. Expect more balanced Budget in February “A good, confidence-inducing Budget, speeding up clearance for projects, and further steps in capital market reforms are required to push up growth.” – Raghuram Rajan, Chief Economic Advisor to Finance Minister. While most are expecting a populist budget in a pre-election year, we expect, the Finance Minister to present a more balanced Budget in February 2013. The current state of weak government finances and, high twin deficits, will make it extremely difficult for the government to present a populist Budget. At the same time, the government would like to take this opportunity to establish its credentials as a reformist government which may provide it with the much needed money for its populist measures. It could also bail out the government from the charges of corruption. The finance ministry is also mulling reducing or all-together abolishing tax on gains arising from transfer of listed securities, whether in the nature of capital gains or business income, for both resident and non-residents. If this happens, it could be an added incentive to the domestic investors to rush into the equity market. Interest rates to tend downwards Unlike the easy money policy pursued by Central Banks in developed economies, in India, RBI has been more concerned about inflation. As a result, there has been no change in policy rates in the last nine months. In its latest policy review, RBI expects headline inflation to ease from the fourth quarter of this financial year starting January 2013. Accordingly, most believe that there is a “reasonable likelihood” of RBI easing interest rates in January – March quarter. With interest rate likely to tend downwards in coming months and quarters, equity automatically becomes more attractive. Lower interest rate normally spurs both investment and consumption. And last but not the least, it reduces interest costs of companies and, thus increases their profits. India Inc looks at consolidation rather than growth After disastrous a FY13 due to a combination of factors like declining GDP growth, persistently high consumer inflation, poor public finances and worsening macro-economic indicators, India Inc is well set to go into a consolidation phase in the months ahead. Most good companies have completed their capex cycle in last few years and do not need to create additional capacity for the next three to four years. Their focus has now shifted to market development, brand building and deepening the sales and distribution network, so that they gain the most when economic growth picks up a few quarters from now. Most feel that economic growth has bottomed out and, unlikely to decline any further. We are likely to see a process of consolidation and, if allowed to play out fully, it will kick-start the next cycle of growth. As one industrialist rightly says: “You can’t wish away 1.2 billion people in India. Most of them still want to build homes, asking for more roads, rail, airports and other physical infrastructure. Growth is only a matter of time.” Performance of QuestPMS After non-too-encouraging performance during FY2012, in the first nine months of FY2013, the performance of QuestPMS has been better. While we may be tempted to pat ourselves on our back, we reiterate that the state objective of QuestPMS is to follow a disciplined process of identifying and investing in companies that should deliver high absolute returns over a 3 to 5 year horizon. The performance table presented below reflects our commitment to achieving our stated objective and we expect to continue to do well in the last quarter of the current year and, in years to come.

Investing early in new bull market and new leadership Normally in the first stage of a bull market, the indices do not make headlines, the news do not make headlines. Internally, the market starts building a base for a greater upmove. And that’s what is happening now. It is only when commodity prices and interest rates start declining, is when you see the second leg of bull market. In our view, the second leg of the bull market, investors may have to wait until February or March 2013 i.e. just around the time the government presents the Budget. Due to high interest rates, slowdown in capital spending and award of projects by the government, the entire infrastructure and related segment was substantially downgraded by the market in last few quarters. Anticipating a fall in interest rates coupled with softening in commodity prices and an increased government emphasis on infrastructure development, we have invested almost a third of the QuestPMS portfolio in companies that operate in infrastructure development, power utilities, transmission towers, engineering and railway products and hydro equipment manufacturing sectors. We expect these companies to do very well in coming year. Conclusion While the recent economic reform push has offered short-term solutions and brought cheer to the capital markets, the country has yet to address other bigger challenges like high inflation, high interest rates, high fiscal deficit and becoming globally competitive. We are living in times, where in most countries in the world, including India, politicians are finding it difficult to take tough economic decisions. Their fear is: it will cost them a lot of votes. Therefore, they push the problems to the future. At a time when global interest rates are almost zero and investors are seeking deploy funds into growth economies, taking baby steps to attract money to cover the current account gap is a short-term solution. The government has to take some strong bottom-up action like cutting wasted subsidies, bring clarity between environment and development and kick start a few infra projects through government owned entities in order to avoid problems of Civil Society and land acquisition. While the market mood has enhanced due to the policy actions taken by government, a lot more needs to be done. And unless those actions are forthcoming, there is always a risk of the mood dampening again. One single action that can maintain the strong sentiment for attracting investment into India is to kick start infrastructure projects. We, at Quest, believe after a long period of policy paralysis, the government has finally woken up. There is a signal that the government is keen on taking decisions and is determined to take reforms forward. We believe, inflation and interest rate cycles are at a peak today and, will slowly but surely reverse in southward direction. We also believe, that the coming fiscal budget will be more pragmatic and the government will try to push growth in the year ahead. Our belief is that recovery can be very fast as fundamentals are strong – we have the demographics, the demand, and the consumption. If we create a facilitative environment, the ability to invest will come back quickly. All this makes us cautiously optimistic on India and Indian markets in the months ahead. We wish you and your family a happy, healthy and a prosperous New Year. Warm regards, Ajay Sheth December 31, 2012 To know more about Quest and QuestPMS please visit our website: www.questinvest.com DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Ajay Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |