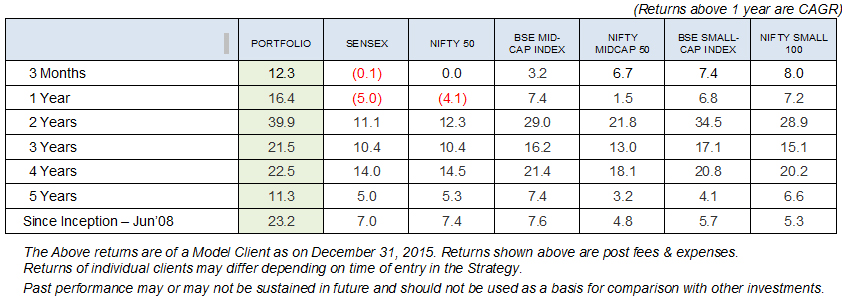

Return to “Fundamentals” driven investing from “Liquidity” driven investing:Calendar 2015 has been a tough year for investors globally with almost all asset classes viz. equities, commodities, bullion and real estate struggling. While developed market equities have been relatively stable, the MSCI emerging market index is down by over 15 per cent, with some markets coming off by over 25 per cent from their recent highs. The world probably has fallen into a deflationary rut with most commodities declining between 20 and 40 per cent during the year. The fragile global economy also forced US Federal Reserve to delay commencement of the monetary tightening cycle to the fag end of the year. However, one expected India to do better following last year’s regime change and improving macro parameters viz. falling interest rates, current and fiscal account deficit, mid-single digit inflation and relatively stable rupee. But Indian markets ended lower for the calendar year. The optimism of a turnaround in corporate performance in India has been tempered by anemic growth in earnings, falling exports and continuing downgrades by the analyst community. Also, we had two below-par monsoons and untimely rains in some parts of the country impacting the rural sector. However, one expected India to do better following last year’s regime change and improving macro parameters viz. falling interest rates, current and fiscal account deficit, mid-single digit inflation and relatively stable rupee. But Indian markets ended lower for the calendar year. The optimism of a turnaround in corporate performance in India has been tempered by anemic growth in earnings, falling exports and continuing downgrades by the analyst community. Also, we had two below-par monsoons and untimely rains in some parts of the country impacting the rural sector. During calendar 2015, Sensex has fallen by 5.0 per cent (from 27,500 to 26,118) and Nifty 50 has fallen by 4.0 per cent (from 8,283 to 7,946). In this backdrop, QuestPMS has appreciated by 16.4 per cent after all expenses and fees. This indicates a swing performance of almost 21 per cent for the year. It is quite apt to quote Howard Marks here: “Our portfolios are set up to outperform in bad times, and that’s when we think our performance is essential. Clearly, if we can keep up in good times and outperform in bad times, we will have above average results over full cycles and below average volatility, and our clients will enjoy outperformance when others are suffering.” We at Quest believe that time has come for “fundamentals” based investing rather than “liquidity” driven investing. The era of easy money making is over. “Stock picking” is going to be the key driver of returns – where QuestPMS has a proven track record. Performance Table:

Our strategy of investing in quality growth companies at an early stage has helped us in delivering compounded annualized returns of ~23 per cent vis-a-vis ~7 per cent for Nifty and Sensex since June 2008. In absolute terms, Rs.1 crore invested in QuestPMS in June 2008 is worth Rs.4.82 crore as on December 31, 2015. For the same period, Rs.1 crore invested in Nifty Index is worth Rs.1.66 crore. To achieve this outperformance, we have followed a rigorous and disciplined process of identifying and investing in good quality and attractively valued businesses. This has been backed by patience of holding them for a period of 3 to 4 years in many cases. Clearly, stock market has again proven that it is a device of transferring wealth from an impatient investor to a patient investor. QuestPMS Fundamentals: QuestPMS portfolio companies’ revenues are projected to grow at CAGR of 14 per cent over the next 3 years (FY15-18), however, due to margin expansion (not only from sharp fall in commodity prices but also leveraging capacity utilization), projected earnings are expected to grow at a substantially higher 29 per cent CAGR over the next 3 years (FY15-18). Our portfolio’s weighted average price-earnings multiple is 18.0 times FY16, 13.1 times FY17 and 10.7 times FY18 earnings. Almost 49% of our portfolio is invested in infrastructure, housing, engineering and related industries which would gain tremendously from government infrastructure spend. These are the companies which have indicated that increased government expenditure would get reflected in their order books over the next two quarters and they will see an expansion in their margins from not only lower commodity prices but also higher capacity utilization. Also, the government’s plan of cutting corporate tax rate to 25 per cent within four years will help our portfolio companies as most pay full tax at the margin. We like to be off the map and assemble a portfolio that’s different from those held by most other investors. Again it is quite apt to quote Seth Klarman here : “In investing – as in most things – people like what is popular, trendy, exciting and dislike what is boring, out of favor and stigmatized. They like assets that have been rising and shun those that have been falling.” Bihar setback – a blessing in disguise? Bihar election’s stunning setback could be a blessing in disguise for Modi. Last 18 months progressive agenda of the Modi government has often been disrupted by the untimely and ill-advised statements of “‘Hindutva” leaders giving fodder to the opposition to obstruct the functioning of the parliament. Bihar elections debacle has pushed Modi to take strong steps towards marginalizing these voices and reaffirming his image as the development and governance-oriented statesman determined to take India forward. The announcements on the FDI front opening up the economy further, immediately post the Bihar elections, and out of box approach towards restarting dialogue with Pakistan are pointers in this direction. At the national level, Brand Modi is still intact, though it may have got frayed at the edges. Modi will be completing 2 years in office in a few months. Most of the real work is done between year two, when the new government has settled down, and year four, after which it gets into election mode again. The 2016 budget might carry Modi’s stamp and he may, in addition to continued focus on infrastructure, recalibrate budget priorities to address those parts of the economy that have been under stress due to two drought years and untimely rains. Further, Modi will continue with the unglamorous work of fixing leaky pipes and enabling ease of doing business. This along with fostering inter-state competition for attracting investments is even more important than the legislative work in the parliament. It will cut corruption and bring jobs quickly by making India attractive to the small entrepreneurs. India’s growth cycle to recover over next few quarters: Hardly any large economy is positioned as attractively as India. It has a new pro-growth government and is at the bottom of an economic cycle. While the overall optimism of the markets have been tempered somewhat in 2015 due to reversals in state elections, dysfunctional Rajya Sabha and slowing global growth, the continued single minded focus of this government towards bringing about structural changes enabling ease of doing business makes us even more bullish with regard to the Indian economy. Almost all the steps taken by the governments viz. e-auctions with respect to natural resources, direct benefit transfer, improving governance at public sector banks, further opening up of the economy, and most importantly, virtual disappearance of corruption at the highest level reaffirms our view that a stage is being set for India to grow at 7.5%+ for many years to come. Fall in commodity prices is a large windfall for India; resources that would have been transferred to the commodity exporting countries are now retained by households, corporates and the government in India. Also, fall in commodity prices has offered India a historic opportunity to build its infrastructure at a much lower cost. Economic growth is poised to accelerate in the coming years though the initial improvement may be uneven and gradual mainly due to external headwinds that the economy is facing. However, cumulative impact of incremental reforms in the Indian economy should result in revival of domestic demand giving confidence to the private sector to initiate the capex cycle in the next 12 to 18 months. Finally, it seems the Gods are also likely to smile on India as El Nino weakens and possibility of La Nina comes to the fore over the next few months. Japanese and European agencies are forecasting the probability of La Nina developing in 2016. India has never had 3 consecutive monsoon failures and hopefully 2016 will see a normal monsoon. This will be crucial as the rural economy has been under stress for some time now and the government can do with some divine intervention here! Risks to outlook: We believe that risks to the India story are more external than internal. After an FII equity inflow of ~ US $16 billion in FY15, last 9 months have seen an outflow of over US $3 billion. This is only the second time (assuming that it doesn’t reverse in the next 3 months) in the last 15 years when the country would see a net outflow of FII equity money. The same is triggered by redemptions from Emerging Market funds which may continue for some time. Also, rise in interest rates in the US can further accentuate the problem. However, the recent performance of the INR confirms that India is perceived to be better positioned, relative to other emerging economies and relative to where it was in 2013 when taper tantrums started. China devalued Renminbi by 4 per cent against the US Dollar in 2015 and it might weaken it further as it transitions its economy from investment to consumption led growth. This can be disruptive for emerging market currencies. Also, while most analysts believe that the real growth in China is lower than the published numbers, the gravity of the problem (slowdown in growth and rise in domestic debt) is still a matter of debate. Further slowdown in China can put more pressure on commodities which can trigger their own set of issues pushing global economy into recession. Final Thoughts: Indian economy is already showing early signs of revival. Introduction of law to ban commercial vehicles that are more than 15 years old (being speculated in the press) can provide further fillip not only to the automobile industry but to the entire Indian economy. The Rs. 40,000 crore National Investment and Infrastructure Fund has evinced strong interest from sovereign wealth funds and pension funds and this could bode well for the infrastructure sector. In our view, all the essential ingredients for “take-off” of the Indian economy (government’s concrete steps towards reforms and ease of doing business, low commodity prices, structural reforms through “Jan Dhan” and direct benefit transfer, etc.) are falling in place. Advent of ‘’normal monsoons” reviving rural economy will be the last element in the jig saw puzzle that will ensure that India moves into a much higher growth trajectory. Stocks, if chosen well, in such an environment will give once in a decade opportunity to generate super normal returns over the next few years. Admittedly, the revival will not be uniform and the divergence between broader market and NSE 50 will continue in 2016 as well. We believe that companies with better earnings visibility will outperform the headline indices. Further, better earnings visibility will also provide cushion against any global shock that one may encounter. We believe that QuestPMS’ portfolio with high earnings visibility is ideally positioned to outperform the markets as it has done across varying time periods in the past. Domestic investors have been investing continuously. They are shifting from physical assets like real estate, gold, etc. to financial assets. We don’t see the commodities recovering anytime soon. We believe inflow of domestic money will be higher than FII money and provide stability to the markets. India is in a sweet spot and equities will do wonderfully well over a period of next 2-3 years. We at QuestPMS are quite excited and the developments of 2015 have reaffirmed our view that India’s time has come. Before I sign off, let me wish all our investors a very happy, healthy and prosperous New Year. Bharat Sheth December 31, 2015 DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Bharat Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and, are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |