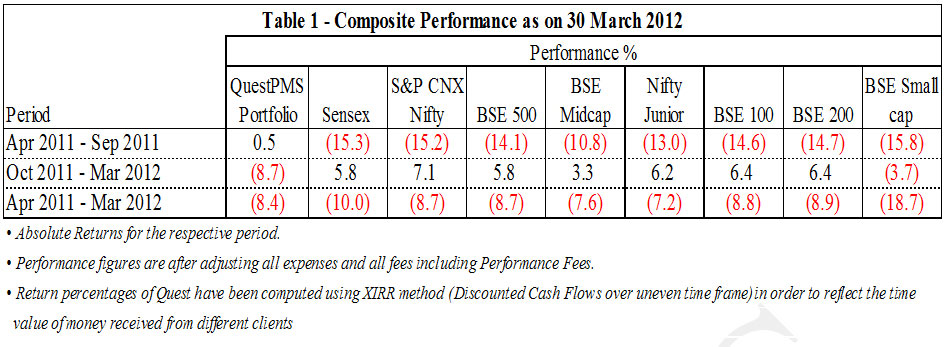

Market at Crossroads: Commodity prices can become the game-changer for IndiaFor the year that has ended, let us start by admitting that we are disappointed with our performance, especially since October 2011. At the beginning of the year, there was a great deal of optimism about India. At the moment, nothing seems to be going right for the Indian markets – be the external factors or resolution of internal issues. The Union Budget was the last glimmer of hope that investors were holding on to – this too faded away with a weak Budget. The retrospective amendments in tax laws announced in the budget have added to the all round confusion. While we may not see any large scale pull out by FIIs, but this could impact fresh inflows. Without being defensive, we urge our investors to read through our critical analysis. In a post budget interview a leading banker summarized the current domestic situation – “The mood right now may not be as glum as we were making it out to be last year but it’s not as positive as it would have been. I believe there is a wall of money sitting offshore that is waiting to come to India. They want to invest, they want a reason to invest, we have to give them that reason and we have not been able to do that in the budget.” India represents a very large opportunity which, in my opinion, no serious company or investor could or would like to miss. Current outlook For India, a sign of recovery in USA is good news. But, Europe is still not out of the woods. China is slowing down and, some expert commentators also expect a hard-landing in China. Despite a forecast of weakness in large global economies, oil, a major commodity imported by both India and China, is ruling firm due to the standoff between US and Iran over the latter’s nuclear aspirations. Internally, we have not seen reforms for the last few years, with the present government becoming weaker and weaker. The other worrying factor has been that inflation has been quite stubborn. This has reduced the possibility of RBI announcing a sharp reduction in interest rates. The third worry is that capital formation has been the lowest in the last decade. And lastly, prediction of weaker monsoon by global agencies, may exacerbate India’s inflation woes and adversely impact the GDP growth resulting in a higher than budgeted fiscal deficit. There is gloom all-around. What can change GLOOM to BOOM for India Policy inaction is a factor that is commonly cited by most investors as the key deterrent to investment flows. At the risk of sounding defensive of government inaction, let me say that the one factor that can change the current gloomy environment in India is a sharp fall in INFLATION. Reduction in inflation can bring a big relief all around. It will help RBI sharply reduce interest rates; it will boost both savings and investments and, it will also bring down fiscal deficit. Lower oil and commodities prices are the key to reducing inflation. While it is very difficult to predict oil and commodity prices, it is clear that high prices of oil and commodities have started affecting global growth. Growth forecasts are being lowered across the globe. Both China and India are expected to grow at a much lower rate as compared to their last few years’ average growth. There are multiple reasons that explain the slowdown. China is purposefully decelerating to a more sustainable growth rate. Its export flows to Europe, and the US are slowing, as the flow of commodities into China. The impact of a slowdown in China – the biggest partner for Brazil, South Africa and other commodity exporters – will be felt across the globe. Despite all these worries, markets have moved up sharply by ~12% in the first quarter of 2012. The genesis of the current risk-on rally is in increased FII flows amidst a belief that the problems in the Eurozone would be resolved and, RBI may start cutting interest rates to boost growth. Ample liquidity has been injected into the system by the loose monetary policy of Central Banks – the Federal Reserve through its QEs, The European Central Bank through the LTRO and, more recently by the Bank of England and Bank of Japan. Some of this low cost money has found its way into global equity and commodity markets. But, a happy co-existence of high prices in both the markets is not sustainable. One of the two has to reverse. The world is passing through turbulent times and, it is hard to believe that it can sustain such high level of oil and commodity prices. It is probable that a slide back into recession or even slower growth can set oil and commodity prices tumbling again, as in 2008. We believe low crude prices are the single most important variable for India to make a comeback as a BOOM economy. Investment Strategy As we see it, the markets are at a very interesting point, seeking direction. What should be the investment strategy during these cyclical swings? Should one continue with the buy and hold strategy? Our two decades of investing experience shows that for the strategy to generate positive returns, it requires patience and discipline. As a core investment thesis we, at Quest, are content to hold the shares for a long period of time as long as the company is creating economic value. We do not panic if the share price declines in the interim. The advantage of this long term investment strategy is that it eliminates, or at least attempts to minimize, the degree to which short term market fluctuation affects an investor’s annual return. But as always, we reiterate, it is futile to predict market cycles. And in any case, we do not buy the market, we buy individual stocks. Also, cycles are inevitable in equity market and it is also a fact that cycles are becoming shorter. “The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions.” – Seth Klarman Performance of QuestPMS We acknowledge that for the just concluded financial year, our performance has been below the standard that we have set for ourselves. To better understand our performance over the last one year, we have critically looked at the performance of QuestPMS broken up into two halves i.e. one upto 30 Sep 2011 and, the other for the second half (see Table 1 below). At the end of Sep 2011, when the benchmark indices were down by 10-15%, at an aggregate level, QuestPMS managed to preserve capital. However in the subsequent six months, our performance has been severely impacted.

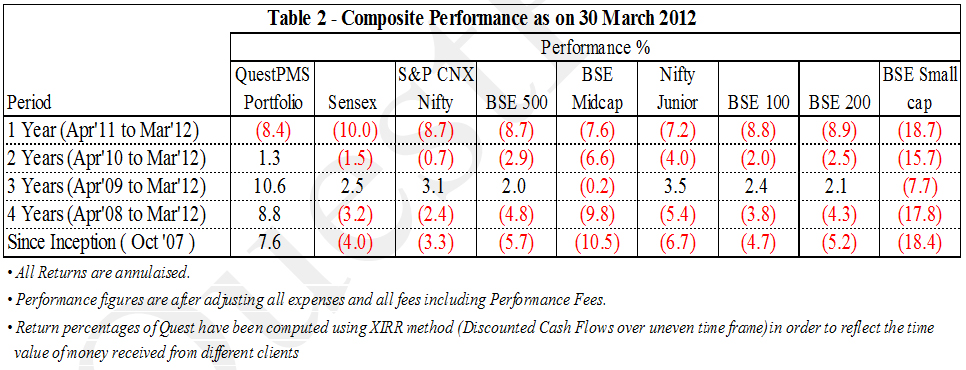

The performance has been impacted not because we deviated from our chosen investment strategy and criteria. There are two primary reasons. In the last three months, due to ample liquidity with FIIs, there has been substantial buying into shares that have a close relevance to specific indices. Also, during this period, the performance of some of our portfolio companies was below our expectations. This impacted the share price of these companies. Despite this, at an aggregate level, for the year ended March 2012, the performance of QuestPMS is just in line with the benchmark indices. The Table 2 given below shows the consolidated performance of QuestPMS and, reflects our commitment to generating absolute returns over the long term:

Our analysis shows that four, out of an average of twenty companies that have been in the portfolio throughout the last year, have contributed substantially to the erosion in value of the portfolio since October 2011. Two of our large positions were impacted by the government’s policy inaction on stimulating investment in infrastructure. The first company – Texmaco Rail, has been impacted due to a delay in receipt of orders from the Indian Railways. Freeze in investments in the power sector due to many regulatory uncertainties such land acquisition, environmental clearances and no assurance on fuel linkage has affected order execution and fresh inflow for Alstom Projects. The third company, RPG Life Sciences that has a valid WHO GMO and a clearance from TGA, Australia, failed to get a clearance of its API facility at Navi Mumbai for exports to some European markets. The company has taken immediate remedial measures and, the results are likely to become evident in the next 2-3 quarters. And the fourth company, Sudarshan Chemcials, witnessed a slowdown in demand – a consequence of the European crisis. The benefit from the large expansion in pigment capacity is not yet reflecting in the performance. In the interim, high interest costs and depreciation has impacted the profits. The issues affecting the respective companies are likely to be resolved in different quarters over the next one year. We emphasize that there has been no change in the competitive environment for these companies, nor is there a change in the management’s approach to conducting the business in a fair and equitable manner. We, therefore, believe that the fall in share price of these companies is reversible. Conclusion As we have opined, for India, the problems are more internal than external. We have a lot going for us if we can get our act together. There is no reason why we should not be growing at 9-10 per cent. We know we can do it and, we just need to seize the opportunity and get there. My team and I will continue to evaluate events as they unfold and, make suitable adjustments to the QuestPMS portfolio. While the market may look hazy in the short run, we believe, that oil and commodity prices could be the game-changer for India in general and stocks in particular. Since July 2011, through these newsletters, we had started a formal communication with our investors in QuestPMS on a monthly basis. Based on our interaction with some of our clients, we have decided to make this formal communication on a quarterly basis. Needless to say, we will write a special letter if any major event unfolds in between the quarters. I conclude with a quote: “I own stocks. I do not trust Treasury Bonds. I had rather have a dividend than coupon. I am afraid of inflation. So I have no choice but to own stocks and some real assets to preserve my financial situation.” – Nasim Taleb, the author of Black Swan. We value your trust and, will strive for your continued interest in QuestPMS. Warm regards, Ajay Sheth March 30, 2012 To know more about Quest and QuestPMS please visit our website: www.questinvest.com DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Ajay Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |