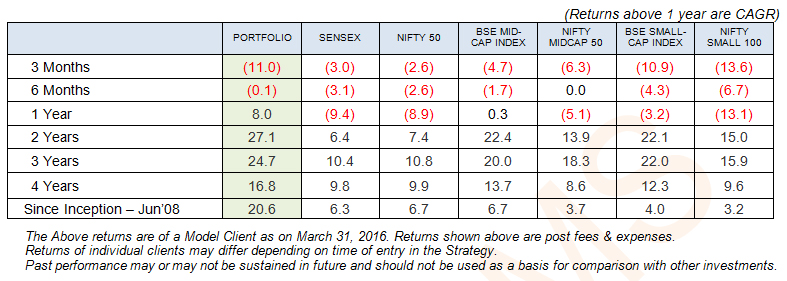

Building blocks in place for India’s economic recovery on a sustainable basisNarendra Modi’s government has presented 3 budgets since coming to power and has brought about significant policy level and on the ground changes during this brief period of less than 2 years. We are convinced that after a long period of 25 years (i.e. after the historic budget of 1991), the Indian economy is witnessing structural changes that can create a basis for India to move into a significantly higher income trajectory (per capital income of $5000+) sometime in the second half of next decade These structural changes entail 4 key initiatives. They include (1) guiding savings of Indians towards productive usages rather than into gold and real estate which accounts for ~70% of all savings (2) disrupting crony capitalism (3) reducing corruption & leakages by significantly improving delivery mechanisms and (4) making it easier for corporates and SMEs to do business by repealing outdated laws, simplifying procedures and providing a framework for resolving disputes. Almost all major campaigns of the government, whether it be e-auction of country’s resources, opening of over 20 crores Jan Dhan accounts, activation of Direct Benefit Transfer, reducing subsidies (-2% CAGR during FY14-16 vis-à-vis 19% CAGR between FY04-14), cleaning of bank’s balance sheet or coming down hard on parallel economy, in one way or the other reinforces these initiatives of the government. The Modi government is not only successfully bringing about the aforesaid changes (~INR 6,000 crore per month already being directly transferred to bank accounts through the Jan Dhan, DBT and Aadhaar mechanism) but has also demonstrated its resourcefulness and innovativeness in resolving vexed issues that have troubled power, roads, railways, defense and oil & gas sectors for many years. It has also displayed its flexibility and thoughtfulness in the most recent budget by focusing on rural and agrarian economy that has been highly stressed due to 2 consecutive monsoon failures and has significantly enhanced investment in productive assets like rural roads and irrigation facilities. We strongly believe that these positive initiatives by the Modi government will have far reaching and long lasting impact on India’s future and place in the global economy. However, these path breaking changes require ‘transition period’ for putting the right systems in place as well as for bringing about change in the mindset of the business community. In the interim, however, short term GDP growth is impacted (as has been the case over the last 12 to 18 months), while the corporate sector gets used to the new rules of business. The structural changes (end of license raj) brought about by the Manmohan Singh’s budget of 1991 took 2-3 years to reflect in higher growth rates for the Indian economy. We believe similar is the case now as well and with every passing quarter, we are reaching closer to the point where the benefits of these structural changes will start becoming apparent to all and will start reflecting in not only the GDP growth rates but also in corporate earnings. Weakness in global economy reflecting in recent market volatility This quarter saw a volatile correction in the markets. Slowing global growth worries were accentuated by further decline in crude oil prices (WTI hit a 12 year low of ~$26 before staging a smart recovery) and rapid depletion of foreign currency reserves in China. Redemptions by sovereign funds (due to low crude prices) led to selling by EM fund managers forcing huge selling in the Indian market in January and February given their overweight stand on India. This unnerved domestic inflows too which were holding up pretty well till then. Sharp increase in slippages in Indian public and private sector banks (triggered by RBI induced cleaning of books) further reinforced the negative sentiments. “Greed and Fear” has always led to disproportionate market movement and this quarter saw these excesses again. However, it is the fundamentals (earnings potential and growth) of companies that finally determine their stock prices and this is what we at Quest concentrate on while being watchful (though not overly concerned) of the short term movement in the prices of our portfolio companies. We at Quest are focused on the big picture and prefer to keep the short term noises / distractions away (these are opportunities as long as they do not impact our big picture). Infact, as portfolio managers, we await periods where fear overcomes greed as these are times when bargains are available even in quality names. Indeed, we have further reduced our cash position during this quarter and we believe that this will hold us in good stead in the medium and long term. Performance Table:

The January to March quarter saw sharper decline in small and mid-cap stocks. While Sensex and Nifty50 were lower by ~ 3%, small and mid-cap indices fell in the range of 5-14%. In line with small and mid-cap indices, Quest’s performance too trailed that of Sensex and Nifty50 during this quarter. However, Quest continues to outperform the market over medium and long term with 1 year, 2 year, 3 year and 4 year returns beating not only Sensex and Nifty50 but also mid and small cap indices by a comfortable margin. Investors who have been with Quest since June 2008 have generated a compounded annual return of ~20% post all fees and expenses during this lean period of almost 8 years for the Indian stock market. India story is not only alive but will soon start kicking India always had the essential ingredients viz. demography and democracy in place for sustained economic growth. However, crony capitalism and all pervasive corruption had impeded the progress and had even led to a sense of despondency in recent years. Change in government at the Centre brought in a sense of optimism and by stroke of luck, a sharp fall in crude prices dramatically improved the macro picture. The need of the hour was to capitalize on this good fortune by focusing on fiscal consolidation, investing in infrastructure and bringing about structural changes in the economy. This is exactly what Suresh Prabhu’s Railway Budget and Arun Jaitley’s Finance Budget has set out to do. They are clearly reflecting the concerns, priorities and programmes of the government. Against a challenging background, both the budgets have, very sensibly, stuck to the basics. The demonstration of commitment to macroeconomic prudence and stability by Jaitley has already softened long term interest rates, bought valuable insurance in an uncertain world and made room for policy interest rate reduction by the Reserve Bank. Prudent government measures such as calibrated increase in MSP for agricultural produce has resulted in food inflation (that had spiraled to mid-teens under the UPA regime) remaining low (5-6%) despite 3 consecutive crop failures. Steps such as 100% FDI in food processing and food retail will ensure that inflation remains structurally low going forward as well. Requirement of PAN for purchases of over INR 2 lacs and imposition of excise duty of 1% on jewelry are attempts to bring the parallel economy into the fold of formal economy. The emphasis on agriculture and rural development is welcome in the context of two bad monsoons. Given the forecast of normal monsoon in 2016 by leading international agencies, we are likely to witness revival in rural demand over the next few quarters. More positively, the large allocations for roads and railways (in the rail budget), coming on the back of similar thrusts in the preceding Budget, should help build decent public investment momentum in these key infrastructure sectors. This can have a multiplier effect on the growth of the economy. As demand picks up and capacity utilization improves due to the aforesaid measures, we will see private capex slowly but surely come back in the next few quarters. Further lowering of cost of borrowing and implementation of sixth pay commission will not only help incentivize demand for consumer durables, automobiles and housing but will also make it easier for corporates to make investment decisions leading to a full-fledged recovery in the Indian economy by FY17-18. Identifying sectors that will drive the market will be key to generating superior returns While there is little doubt in our minds that we are very close to a sustained recovery in the Indian economy, we believe that identifying the sector(s) that will take leadership in the next phase of the market will be key to generating superior returns for investors. History tells us that leadership changes in every market cycle and the sectors that lead the market give super normal return during that period. We have seen leadership shift from ‘old economy’ stocks to IT sector in the mid and late nineties and then to capex related sectors in the 2003-2008 period when the Indian market saw its biggest bull run till date. The leadership again shifted to consumer, IT & pharma during the 2009 to 2014 phase and we believe it is time for a new sector to take leadership and drive the market into the next decade. We at Quest believe capex and infrastructure related companies, particularly in roads, power T&D, railways, etc. with reasonably healthy balance sheets should do very well in coming years. These sectors viz. transportation (roads, railways, ports and shipping) and power are likely to witness potential investment of ~ USD 500 billion by 2022 and should therefore play a key role in sustaining India’s GDP growth at 8%+ for many years. We believe that all the right ingredients are in place; there is clear government commitment towards significantly higher infra spends, policy framework has improved resulting in lower risks in execution, governance norms and processes are improving in select infra / capex related companies, competitive intensity is reducing in large and complex projects, softer interest regime is becoming a reality and funding options are increasing thanks to government’s initiatives. Infra, engineering and capex related companies have a weightage of ~45% in our portfolio and we believe that we are well placed to benefit from the surge that we expect in this sector. We continue with our ‘bottoms up’ approach to stock picking with added emphasis on sectors that we believe will benefit from government’s plans and priorities. We have selectively invested in companies that will benefit from government’s push to the rural and agrarian economy as also in sectors like chemicals and textiles where we believe India’s relative competitiveness is improving vis-à-vis China. The weighted average EPS of Quest PMS portfolio is projected to increase at a CAGR of ~27% over FY15-18 and the portfolio is currently trading at a P/E multiple of ~10 on FY17-18 basis. This strength in earnings growth and very reasonable valuations makes us confident that we will continue to outperform the market over medium and long term. Risks to outlook We continue to maintain that risks to India are more external than internal. Most large economies are suffering from anemic growth, ever increasing debt and very low to negative interest rates. Worryingly, most of them have already used the fiscal and monetary arsenal at their disposal and can now do very little to stimulate growth. Further, the twin risks of continued fall in foreign currency reserves in China and another sharp dip in oil prices and consequent redemption pressure may continue to weigh on the Indian markets. However, India being a consumer and hence a beneficiary of low crude and commodity prices should at some point demerge from the Emerging Markets. Local risks primarily pertain to the fragile asset quality of public sector and large corporates focused private sector banks. While the clean-up exercise has begun, it will be a painful process and will keep the profitability of banks under pressure for quite some time to come. Vested interests, impacted by the government’s attempt to reform the system, will also place hurdles on the way and the government’s ability to successfully tackle them will be critical in ensuring a smooth transition. Besides, several industries are today facing heightened risks of disruptive innovations which are changing the dynamics of several businesses and in some cases even making certain businesses / products / services redundant. Successfully navigating through such disruptive innovations (by avoiding companies that may get impacted) will also play a role in the returns that investment managers will generate for their clients in the medium term. Addition to team at Quest Before I come to my final thoughts, let me welcome my new colleagues on board. We have inducted two senior professionals: Jayesh Shah, CIO (with over 25 years of equity sales and research experience at HSBC, Merrill, Deutsche where he was servicing India’s top global investors) and Sandeep Baid, Head – Research (with 18 years of investment banking and private equity experience at organizations such as Rabo India, YES Bank and Citi Venture Capital International). Induction of Jayesh and Sandeep will add to our existing capabilities and should help us serve you better. Final Thoughts It took India 60 years to become a USD 1 trillion economy, while the next trillion came in 7 years. India has the potential to again double its economy (grow into USD 4 trillion economy) in the next 6-7 years. To achieve the same, PM Modi is putting our house in order by improving the fiscal situation, channelizing our savings towards productive assets and building a transparent system that is based on meritocracy. We believe that if the government continues on its laid out path of structural reforms, we will see a very different India in a few years; an India where ‘execution capability’ rather than ‘right connections’ are the basis for doing business, where efficiency and productivity are rewarded and where there is predictable regulatory and taxation regime. We will also see an India where the benefits of growth are much more wide spread, leakages are minimal and people at the bottom of the pyramid actually get the benefits that are intended for them. It is typically the darkest just before dawn and we believe that we went through that period in the recent months. The signs of dawn are becoming visible in the form of green shoots in several sectors. We are already witnessing increasing activity levels in roads, railways, power transmission and now distribution segment with initial success of ÚDAY’. We also believe that by September 2016, the number of Congress MPs in Rajya Sabha will come down and the NDA government will be able to coordinate much better with the other opposition parties on important legislative matters. Whilst the markets have been marred by intense risk aversion over the last few months, India is today like an oasis in a desert. Unlike the developed economies that have adopted short term measures through their central banks to prop up the growth rates, India has taken a very comprehensive approach of a paradigm shift in policies that will reinvigorate growth engines, deal with aggregate demand imbalances and address pockets of stress (excessive leverage). Please note that while ‘hot’ money (read FII) has seen an outflow of ~ USD 3 billion in FY16 due to redemption pressure from sovereign funds, India has witnessed highest ever ‘long term’ FDI inflow of over USD 31 billion in the first 10 months of FY16. Clearly, the work that is being done by this government is being recognized globally, and sooner than later, it will also start reflecting in the capital markets. We are turning more optimistic on the prospects of corporate earnings. Corporate profits (BSE 500) at just over 3% of GDP (5.5% in FY08) is at the lowest level in the last 10 years. We believe Indian companies are likely to register better earnings in the coming quarters due to a positive base effect as also benefit from lower interest rates and input prices. We believe that companies that have demonstrated long-term vision, industry leading expertise, healthy balance sheet and execution capability will do particularly well in the foreseeable future. We strongly believe in the words of John Templeton: “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria”. Investing now could be the trade of the decade. Bharat Sheth March 31, 2016 DISCLAIMER: This communication does not constitute or form part of any offer or recommendation or solicitation to subscribe or to deal with QuestPMS. The views expressed by Bharat Sheth, Portfolio Manager QuestPMS are his personal views as on the date mentioned. These should not be construed as investment advice to anyone. This communication may include statements that may constitute forward looking statements. The statements included herein may include statements of future expectations and, are based on the author’s views, observations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ substantially or materially from those expressed or implied in such statements. The author does not undertake to revise the forward looking statements from time to time. No representation, warranty, guarantee or undertaking, express or implied is or will be made. No reliance should be placed on the accuracy, completeness or fairness of the information, estimates, opinions contained in this communication. Before acting on any information contained herein, the readers should make their own assessment of the relevance, accuracy and adequacy of the information and seek appropriate professional advice and, shall be fully responsible for the decisions taken by them. |